Blog

Blog FAQ’s

FAQ’s What we do

What we do Partner with us

Partner with us Careers

CareersApr 16, 2024

6 min read

Boost Your Business with No-Credit-Check Financing

In the dynamic landscape of business expansion and seizing novel opportunities,...

Read story

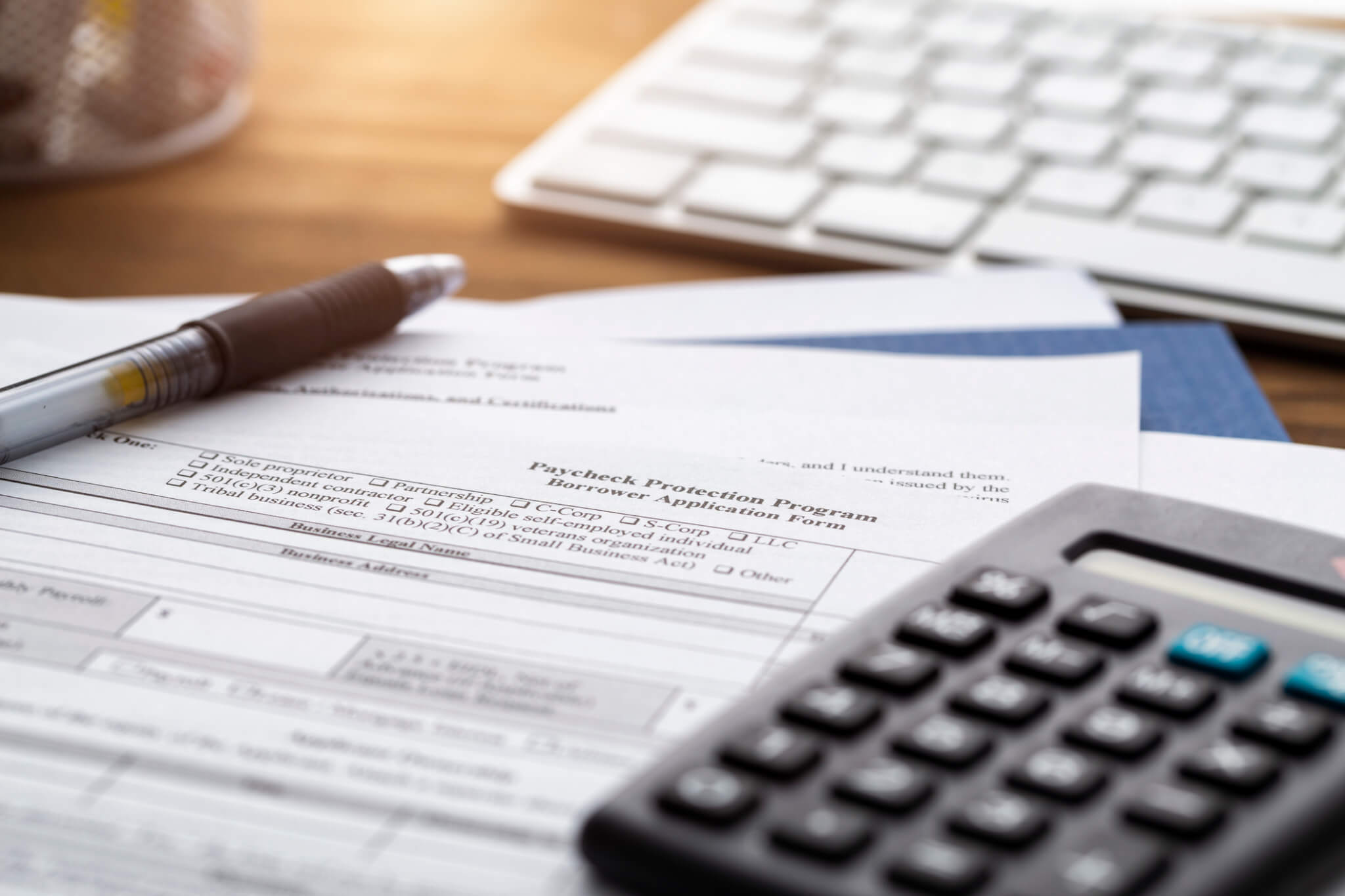

Times are rough. If you haven’t already, you should be looking at programs that allow you to get cash quickly. One of those programs is the Paycheck Protection Plan, or PPP, which is part of the stimulus package recently passed in Washington. Another option is applying for an SBA Economic Injury Disaster Loan, which offers grants of up to $10,000 as well as loans with low interest rates.

As the federal government, banks and other lenders work to distribute money provided by the Coronavirus Aid, Relief, and Economic Security (CARES) Act stimulus package, let’s discuss how to use the money when you receive it.

The primary purpose of the Paycheck Protection Plan is to protect workers. The government wants you to keep your employees on payroll and hire back the ones you let go because of the effects of COVID-19. In fact, if you put your PPP money toward payroll, you may not have to pay it back – ever. You’ve probably heard this referred to as loan forgiveness. “Forgiveness” means that you don’t have to pay back the money you borrowed.

There are some rules you have to follow, though, to have your PPP loan fully forgiven:

Make sure to track you use of the money, so you can prove you used it in accordance with the rules. Go ahead, ask:

Gross salary, wages, commissions, and tips, as well as benefits for employees whose principal residence is in the United States.

If you rehire them at the same or higher salary, they count toward the rules that allow forgiveness of the loan.

They’re not considered payroll costs for the PPP, because they aren’t employees. They can apply for their own PPP loans.

You’ll have to pay it back. But the interest rate is only 1%, and you won’t have to start making payments for six months. The loan matures in two years.

See how SBG Funding can help you with the Paycheck Protection Program (PPP).

How will you spend money from your SBA Economic Injury Disaster Loan?

These working capital loans, including the grant, may be used only to pay fixed debts, payroll, accounts payable, and other bills you could have paid if the disaster hadn’t occurred. The loans are not intended to replace lost sales or profits or to pay for expansion. And you can’t use the money to pay down long-term debt or to consolidate debt.

If you receive a grant, you don’t have to repay it. And the loan will have a low interest rate and a long term, so you can use the money for a long time.

One approach to spending money is to manage your biggest risks and keep your biggest advantages. If you can avoid a serious situation, like losing a supplier or wasting inventory, consider using the grant to save those situations. If you have star employees or other assets that are key your business’s success, see if money can help you maintain those advantages. A bonus can keep someone from quitting. If you’re known for a specific product, like the best croissants, maybe you can dream up a new variety that will further endear you to customers.

Or, prioritize your spending by what keeps you up at night. Paying for the things that are burdening your mind will free up your energy and creativity to think about ways to cope overall.

Speaking of which, remember to consider the longer-term effects of how you use your money today:

Back to basics: Is it time to scale back to the essential purpose of your business and do away with add- ons? For instance, if you’re a gym that has a snack bar, ask yourself: Is your money better spent on new gym equipment, or is offering food is a way for your members to feel fully nurtured by their visits?

Review your regrets: Now that you’ve experienced a big hit on your business, are there things that you wish you hadn’t done? No need to kick yourself. Just be honest, learn from mistakes, fix the situation and be ready for the next phase of life as a business owner.

Evaluate your customers: Ask yourself how you think this pandemic will change the habits of those who patronized your business. If you’re still open, look for clues in how they shop. If you’re closed, use your business wisdom to imagine how people will view what you have to offer when you can open your doors again.

Prepare for the next crisis: What can you do to be ready for the next big curve ball? Is your technology secure? Is your business model sound? Are your risks spread widely enough that you can recover quickly? Some companies draw up a business resiliency plan that considers many awful scenarios and how they will respond to them. It takes a lot of thinking and planning, but it will probably be worth it.

Think about local support: Did your neighboring businesses support you during this hard time? If they didn’t, it could be a sign that you should build alliances with fellow business owners, including your competitors. That could prove valuable in everyday business as well as during crises.

Apr 16, 2024

6 min read

In the dynamic landscape of business expansion and seizing novel opportunities,...

Read story

Apr 16, 2024

5 min read

The journey through the financial realm can be complex for those...

Read story

Mar 05, 2024

5 min read

Starting and growing a business requires immense working capital reserves, and...

Read story

A funding specialist will get back to you soon.

If you can’t hang on then give us a call at (844) 284-2725 or complete your working capital application here.